Ready to make your dream property a reality? Understanding how to get your property finance approved is the crucial first step.

Without the right approval, even the best property deals can slip through your fingers. This guide breaks down the approval process into simple, clear steps so you know exactly what to do—and what to avoid. Whether you’re buying your first home or investing in real estate, you’ll discover how to strengthen your application, gather the right documents, and approach lenders with confidence.

Keep reading to unlock the secrets that can save you time, reduce stress, and increase your chances of approval. Your journey to owning property starts here.

Preapproval Basics

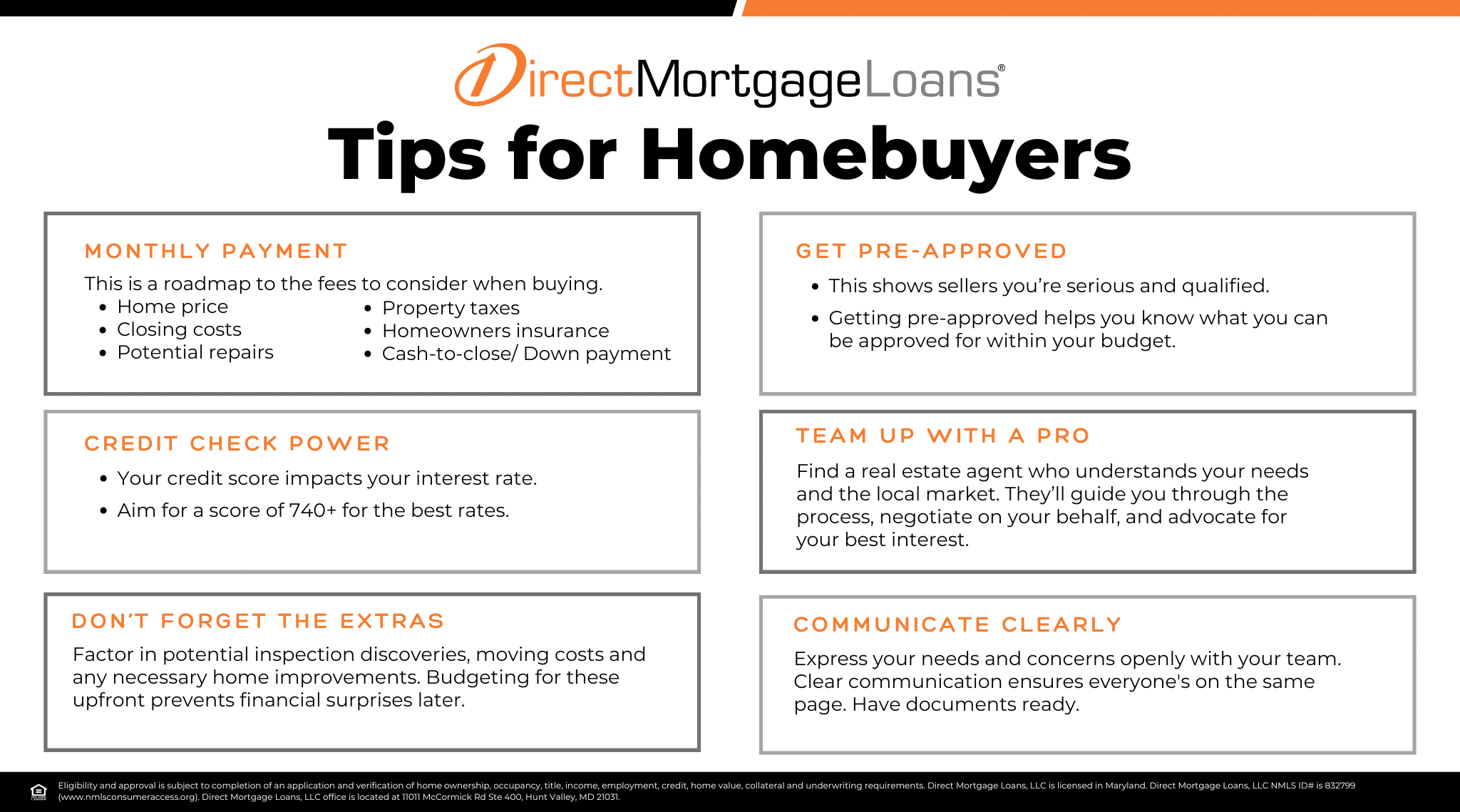

Preapproval means a lender checks your credit and income. This shows how much money you can borrow. Prequalification is less formal and only gives a rough idea of your budget.

Benefits of preapproval include knowing your price range. It makes sellers trust you more. You can act fast when you find a home you like. This can give you an edge in a competitive market.

Preapproval usually lasts about 60 to 90 days. After that, you may need to update your information. Keep your financial documents ready to renew it quickly.

Income Requirements

Qualifying income sources include wages, salaries, bonuses, and commissions. Lenders also accept rental income and some government benefits. Documentation must prove the income is steady and likely to continue.

Income documentation needed varies but commonly includes recent pay stubs, tax returns, and bank statements. For salaried workers, two years of W-2 forms are typical. Self-employed borrowers need profit and loss statements plus tax returns.

Self-employed income tips suggest showing consistent earnings over two years. Keeping detailed records helps. Lenders look for stable or growing income trends. Avoid large unexplained deposits in bank accounts, as this can delay approval.

Credit Score Insights

Credit score is a key number lenders check for property finance. Scores usually range from 300 to 850. Scores above 700 are seen as good. A higher score means better chances for approval and lower interest rates.

To improve your credit quickly, pay bills on time and reduce debt. Avoid opening many new credit accounts at once. Check your credit report for errors and fix them fast.

Common credit pitfalls include missing payments, maxing out credit cards, and closing old accounts. These actions can lower your score and hurt your approval chances.

Asset Verification

Acceptable assets usually include savings accounts, stocks, bonds, and retirement funds. Some lenders accept real estate or valuable personal property as well. Showing assets helps prove financial strength.

Most lenders want to see enough assets to cover down payment, closing costs, and reserves. The amount depends on the loan type and lender rules. It is important to have clear proof of these funds.

Common documents for asset verification include bank statements, investment account statements, and retirement fund summaries. Statements should be recent, usually within 30 to 60 days. Keep these papers organized and ready to submit.

Essential Documents

Valid ID such as a driver’s license or passport is necessary. Lenders use this to confirm your identity and age. Personal information like your Social Security number, date of birth, and current address must be accurate and up to date.

Financial statements include bank statements, tax returns, and proof of savings. These show your ability to manage money and repay the loan. Lenders want to see consistent income and savings history.

Employment verification proves your current job status. This can be pay stubs, employer letters, or contracts. Stable employment shows lenders you have a steady income source.

Choosing The Right Lender

Shopping multiple lenders helps find the best loan for you. Comparing offers can save thousands. Look at interest rates, fees, and loan terms closely. Some lenders may charge hidden fees. Others offer lower rates but higher fees.

Ask lenders important questions like:

- What is the interest rate and is it fixed or variable?

- Are there any application or closing fees?

- How long does approval take?

- What documents are needed?

- Are there penalties for early repayment?

Keep notes to compare lenders easily. Remember, the right lender makes a big difference in your loan experience.

Application Strategy

Start your property finance application early to avoid last-minute stress. Gathering all necessary documents takes time. Early action helps you compare lenders and find the best terms.

Avoid common mistakes like submitting incomplete information or missing deadlines. Double-check your application for accuracy. Mistakes can delay approval or cause rejection.

Respond quickly to conditional approvals. Lenders often ask for extra documents or clarifications. Providing these fast keeps the process moving smoothly and increases your chances of final approval.

Speeding Up Approval

Keep all important documents ready before applying. These include pay stubs, tax returns, bank statements, and ID proofs. Organize them in one folder for easy access. This saves time and avoids delays.

Stay financially stable. Avoid taking new debts or making large purchases. Lenders look for steady income and low debt. Consistent financial behavior helps speed approval.

Talk clearly and often with your lender. Respond quickly to their requests. Ask questions if you do not understand. Good communication helps avoid misunderstandings and keeps the process moving.

Frequently Asked Questions

What Is The 3 7 3 Rule In Mortgage?

The 3-7-3 rule in mortgage means lenders typically take 3 days to process, 7 days to underwrite, and 3 days to close a loan.

How Much Do I Need To Make To Get Approved For A $400,000 Loan?

To get approved for a $400,000 loan, you typically need an annual income of about $80,000 to $120,000. Lenders consider credit score, debt-to-income ratio, and down payment too. Exact requirements vary by lender and loan type.

What Are The 4 C’s That Lenders Are Looking At?

Lenders evaluate the 4 C’s: Credit, Capacity, Capital, and Collateral. Credit shows your credit history. Capacity measures income and debt. Capital refers to savings and assets. Collateral is the property securing the loan.

What Is The 2% Rule For Refinancing?

The 2% rule for refinancing means your new monthly mortgage payment should be at least 2% lower than your current payment. This helps justify refinancing costs and ensures savings.

Conclusion

Getting property finance approval takes careful planning and preparation. Know your income, credit score, and assets clearly. Gather all necessary documents before applying. Shop around and compare offers from different lenders. Start the process early to avoid last-minute stress. Being organized helps you move faster and smarter.

With the right steps, approval becomes easier to achieve. Stay patient and focused throughout your journey. Your dream property is within reach. Keep learning and asking questions to stay confident.