Thinking about buying a home but unsure where you stand financially? Knowing your home loan qualification estimate is the first step to turning your dream into reality.

This estimate gives you a clear picture of how much you can borrow based on your income, debts, and credit. By understanding your qualification estimate, you can shop smarter, avoid surprises, and focus on homes within your reach. Keep reading to discover simple ways to calculate your home loan qualification and gain confidence in your homebuying journey.

Home Loan Basics

A home loan qualification estimate shows how much money a lender might lend you. It helps buyers know their budget before house hunting. This estimate considers your income, debts, credit score, and down payment. Lenders use it to check if you meet their rules.

Knowing this estimate is important. It saves time by focusing on homes you can afford. It also helps you plan your finances better. Sellers prefer buyers with a pre-qualification. It shows you are serious and ready to buy.

Many websites offer free calculators for a quick estimate. You enter simple details like income and monthly bills. The tool then gives you a rough loan amount. This helps you understand what price range to consider.

Key Factors Affecting Qualification

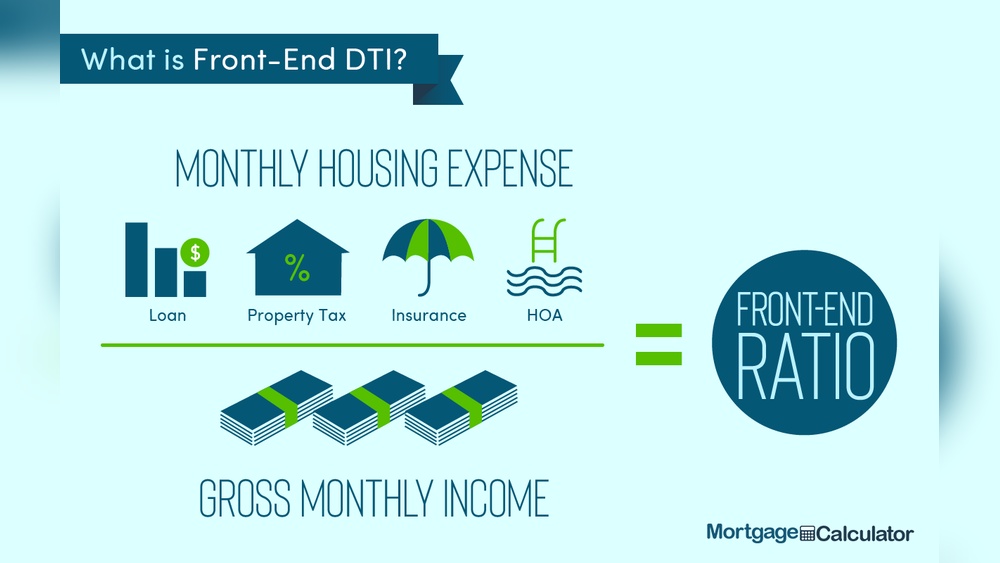

Income and employment show lenders how much money you earn and your job stability. A steady job with a good salary improves your chances of approval. Credit score and history tell lenders how well you pay back money. Higher scores mean lower risk and better loan terms. Debt-to-income ratio compares your monthly debts to your income. Lenders want this ratio to be low, usually under 43%. It shows you can handle new debt payments.

Down payment amount affects your loan size and interest rate. Bigger down payments lower your loan amount and may get better rates. Some loans need at least 3% down, but 20% is best to avoid extra fees.

Using Affordability Calculators

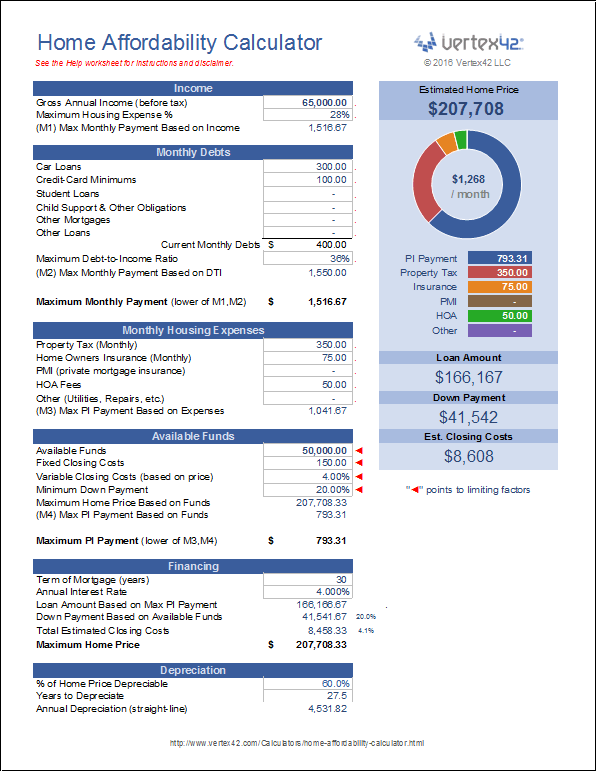

Affordability calculators help estimate the amount of home you can buy. They use your income, debts, and down payment to give a rough figure. You enter simple details like salary and monthly bills. The calculator then shows your maximum loan amount and estimated monthly payment.

Popular tools include options from Fannie Mae, Zillow, Navy Federal, U.S. Bank, and Chase. These websites offer free calculators that are easy to use. Each tool may ask for slightly different information but the goal is the same.

Results show loan size, interest rate, and monthly payments. Use this info to decide what house price fits your budget. Remember, calculators provide estimates, not final approvals. They help you plan before talking to a lender.

Improving Your Qualification Chances

Boosting your credit score helps lenders see you as a safe borrower. Pay bills on time and keep credit card balances low. Avoid opening many new accounts quickly. These steps raise your score and improve loan chances.

Reducing monthly debts frees up money to pay your mortgage. Pay down credit cards and loans before applying. Less debt means a better debt-to-income ratio, which lenders prefer. This makes loan approval easier.

Saving for a larger down payment lowers the loan amount needed. It shows financial discipline and reduces lender risk. Aim for at least 20% down to avoid extra fees. Larger down payments also mean lower monthly payments.

Common Mistakes To Avoid

Overestimating your budget can lead to serious problems. Many think they can afford more than they really can. This mistake causes stress and financial trouble later. It’s smart to be realistic about income and expenses.

Ignoring additional costs is common but risky. Buying a home involves more than just the price. Taxes, insurance, repairs, and utilities add up fast. These extra costs must be counted in your budget.

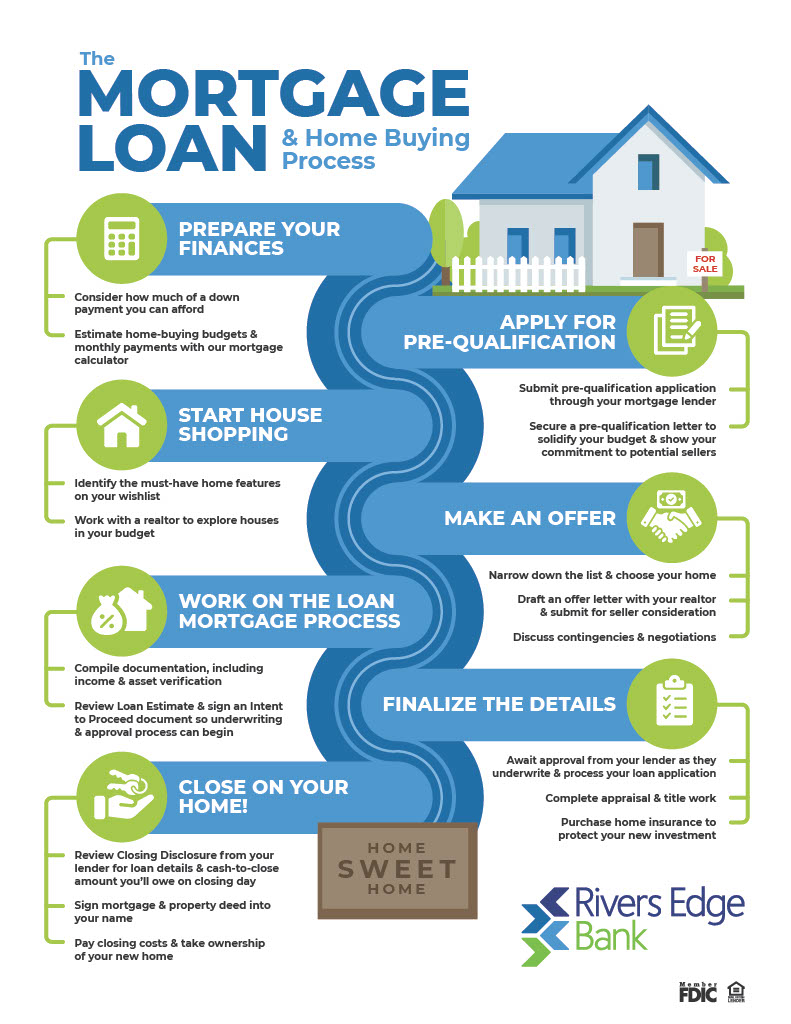

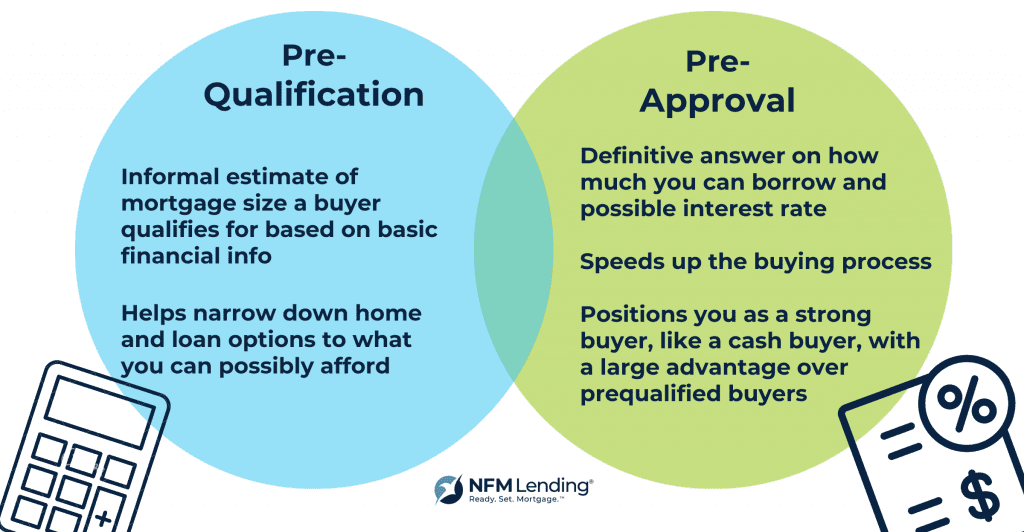

Skipping pre-qualification wastes time and effort. Pre-qualification shows how much a lender will likely lend you. It helps avoid searching for homes that are too expensive. Getting pre-qualified gives a clear idea of your price range.

Local Insights For Austin, Texas

The Austin, Texas housing market shows steady price growth. Median home prices hover around $450,000, with demand rising due to job opportunities and city growth. Neighborhoods like South Congress and East Austin attract many buyers. Local lenders often offer competitive rates and flexible loan options. Some banks provide special programs for first-time homebuyers in Texas.

Homebuyers should check their credit scores before applying. Saving for a down payment of at least 5% to 20% helps secure better loan terms. Texas offers unique lending options such as Texas Veterans Land Board loans for veterans. Consulting with local mortgage advisors can improve qualification chances.

- Review your monthly income and debts carefully.

- Consider loan types: FHA, VA, conventional loans.

- Prepare documents like tax returns and pay stubs.

- Understand closing costs and property taxes in Austin.

Next Steps After Qualification

Getting pre-approved helps you know your loan limit before house hunting. It shows sellers you are serious. Pre-approval needs documents like income proof and credit checks. This step speeds up buying once you find a home.

Starting your home search means knowing your budget and needs. Use online listings and visit open houses. Make a list of must-haves and nice-to-haves. Stay realistic about what fits your price range.

Working with real estate professionals can make buying easier. Agents know local markets and negotiate well. Choose someone who listens and understands your goals. They guide you through paperwork and deadlines.

Frequently Asked Questions

What Factors Affect Home Loan Qualification Estimates?

Home loan qualification depends on income, credit score, debts, and down payment. Lenders also consider employment history and loan type. These factors help estimate how much you can borrow.

How Can I Calculate My Home Loan Qualification?

Use an online mortgage qualification calculator. Input your income, debts, credit score, and down payment. The tool estimates the loan amount you may qualify for based on current lending criteria.

Why Is Credit Score Important For Home Loans?

A good credit score indicates reliability to lenders. Higher scores often lead to better interest rates and loan approval chances. Low scores may limit loan options or require higher down payments.

How Does Debt-to-income Ratio Impact Qualification?

Lenders use debt-to-income (DTI) ratio to assess your ability to repay. A lower DTI means you have enough income to cover debts and mortgage. Most lenders prefer a DTI below 43%.

Conclusion

Estimating your home loan qualification helps set realistic buying goals. Knowing your budget keeps house hunting focused and stress-free. Use simple calculators to check your affordability quickly. Keep track of your income, debts, and savings for accuracy. Remember, better preparation leads to smoother loan approval.

Start early and stay informed to make smart decisions. Your path to homeownership becomes clearer with each estimate. Take control and plan wisely for your dream home.