Thinking about an interest-only mortgage? Understanding the current interest-only mortgage rates is key to making a smart financial decision.

You might be wondering how these rates work, whether they can save you money, or how they compare to traditional loans. This article will guide you through everything you need to know about interest-only mortgage rates—breaking down complex terms into clear, simple explanations.

By the end, you’ll have a solid grasp of whether this type of mortgage fits your financial goals and how to find the best rates available. Keep reading to discover how you can make your home financing work smarter for you.

Interest-only Mortgage Basics

Interest-only mortgage rates let borrowers pay only the interest on their loan for a set time. During this period, monthly payments are usually lower since you don’t pay the loan’s principal.

After the interest-only period ends, payments increase because you start repaying the principal too. These loans suit people who expect higher income later or want lower initial payments.

- Fixed-rate interest-only loans: Interest rate stays the same during the interest-only term.

- Adjustable-rate interest-only loans (ARMs): Rate changes based on market conditions after the initial period.

- Hybrid interest-only loans: Combine fixed and adjustable rates, often fixed first, then adjustable.

Current Interest-only Rates

Average interest-only mortgage rates today range from about 3.5% to 4.5% for the initial term, usually two years. These rates are often lower than traditional mortgages since you pay only the interest, not the principal.

Factors affecting these rates include your credit score, loan amount, and market trends. Lenders also consider the property’s value and your income stability. Rates can change depending on the economy and Federal Reserve policies.

| Lender | Initial Rate | Initial Term | APR |

|---|---|---|---|

| Charles Schwab | 3.59% | 2 years | 7.79% |

| Guaranteed Rate | 3.64% | 2 years | 8.59% |

| Wells Fargo | 4.19% | 2 years | 8.07% |

| Bankrate | 4.54% | 2 years | 6.63% |

Advantages Of Interest-only Mortgages

Lower initial payments make interest-only mortgages attractive. Borrowers pay only the interest for a set period, reducing monthly costs. This helps keep budgets flexible and eases financial pressure early on.

Cash flow benefits allow homeowners to use extra money for other needs. This can include savings, investments, or paying off higher interest debts. It helps manage finances better during the initial loan period.

Flexibility in financial planning is a key advantage. Borrowers can decide how to handle principal payments later. It suits those expecting income growth or planning to sell or refinance before principal payments start.

Drawbacks To Consider

No Principal Reduction means monthly payments only cover interest. The loan balance does not decrease. Borrowers must pay the full amount later. This can cause large payments after the interest-only period ends.

Higher Future Payments happen because once principal payments start, monthly bills rise. Payments might become difficult to afford if income stays the same or drops.

Potential for Increased Costs exists. Interest-only loans sometimes have higher interest rates. Also, borrowers may pay more in interest over time since the principal stays the same longer.

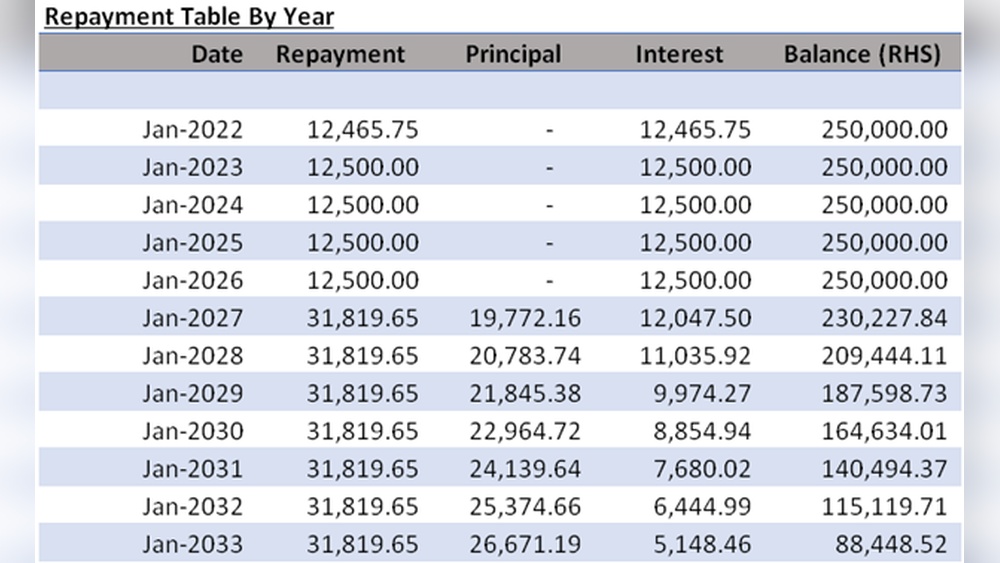

Calculating Interest-only Payments

Using online calculators helps find the monthly interest-only payment quickly. Enter the loan amount, interest rate, and loan term. The tool calculates the payment based on these numbers. It saves time and avoids manual errors. Many websites offer free calculators for this purpose.

Comparing interest-only loans with traditional loans shows key differences. Interest-only loans require payments on the interest only, not the principal. This makes monthly payments lower at first. Traditional loans require payments on both principal and interest, so monthly payments are higher. Over time, interest-only payments may increase once the principal payments start.

| Feature | Interest-Only Loan | Traditional Loan |

|---|---|---|

| Monthly Payment | Lower (interest only) | Higher (principal + interest) |

| Payment Period | Interest-only for a set time | Full payment for entire loan term |

| Principal Paid | After interest-only period ends | Throughout the loan term |

Interest-only Loans In Austin, Texas

Austin, Texas shows varied interest-only mortgage rates based on current market trends. Rates typically range from 3.5% to 4.5% for a 2-year initial term. These loans require paying only interest initially, reducing monthly payments.

Local lenders include Charles Schwab, Guaranteed Rate, and Wells Fargo. They offer competitive rates, often adjusted by borrower credit scores and market changes. Many loans use adjustable-rate mortgages (ARMs) during the interest-only period.

| Lender | Initial Rate | Initial Term | Typical APR |

|---|---|---|---|

| Charles Schwab | 3.59% | 2 years | 7.79% |

| Guaranteed Rate | 3.64% | 2 years | 8.59% |

| Wells Fargo | 4.19% | 2 years | 8.07% |

Making Smart Choices

Evaluating your financial situation helps decide if an interest-only mortgage fits your needs. These loans let you pay just the interest for a set time, lowering monthly payments.

Choose interest-only if you expect higher income soon or plan to sell before the principal payments start. This option suits those with stable finances and good credit scores.

Tips for negotiating rates:

- Shop around and compare offers from several lenders.

- Ask about introductory rates and how long they last.

- Check if rates can change and by how much.

- Show proof of steady income to get better terms.

- Consider locking your rate if rates are low.

Frequently Asked Questions

What Is The Current Average Interest-only Mortgage Rate?

The current average interest-only mortgage rate ranges between 3. 5% and 4. 5% for a two-year introductory period. Rates vary by lender, credit score, and market conditions. Always compare offers to find the best rate for your financial situation.

Are Mortgage Rates Going To 4%?

Mortgage rates may approach 4%, but they fluctuate based on economic trends and Federal Reserve policies. Stay updated regularly.

Are Banks Still Offering Interest-only Mortgages?

Yes, some banks still offer interest-only mortgages, but they are less common and often have stricter requirements.

How Can I Get A 3% Mortgage Interest Rate?

Secure a 3% mortgage rate by having excellent credit, a large down payment, and shopping multiple lenders. Consider adjustable-rate mortgages and government-backed loans.

Conclusion

Interest-only mortgage rates can offer lower initial payments. This may help manage your monthly budget better. Keep in mind, you pay only interest, not the loan balance. After the interest-only period, payments usually increase. Always compare rates and terms from different lenders.

Understand how your finances will change over time. Use calculators to see future payment impacts. Choosing the right mortgage means balancing short-term ease and long-term costs. Stay informed and make decisions that fit your goals.