Thinking about refinancing your mortgage? Before you make any decisions, it’s crucial to understand how long it will take for your refinance to actually start saving you money.

That’s where a Refinance Break Even Calculator comes in. This simple tool helps you figure out the exact point when the costs of refinancing are covered by your monthly savings. By knowing your break-even point, you can avoid costly mistakes and make smarter financial choices.

Keep reading to learn how this calculator works and why it’s an essential step before refinancing your home loan.

Refinance Break Even Basics

Key factors that affect the break-even point include interest rates, loan terms, and closing costs. Lower interest rates can save money each month, but closing costs add upfront expenses. The length of the loan term changes how long it takes to recover those costs.

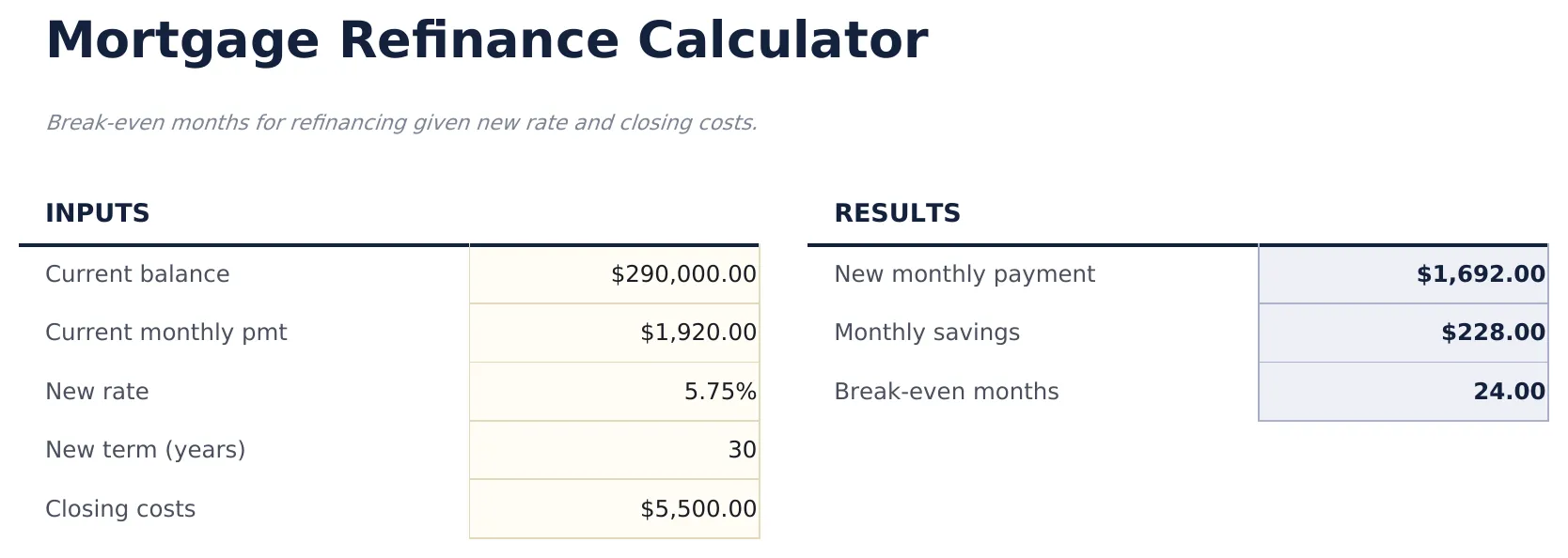

The break-even point is found by dividing total closing costs by monthly savings. For example, if closing costs are $3,000 and monthly savings are $150, the break-even time is 20 months.

Knowing this helps homeowners decide if refinancing makes sense. It can prevent costly mistakes and show how soon savings start to add up.

Using A Break Even Calculator

To use a refinance break even calculator, enter some key numbers. These include the current loan balance, interest rates of old and new loans, and the closing costs for refinancing. Also, provide the monthly payment amounts of both loans.

The calculator finds how long it takes to recover the refinancing costs. This is called the break-even point. It shows the number of months needed to save enough on monthly payments to cover the closing costs.

Results help decide if refinancing is smart. If the break-even time is short, refinancing might save money soon. If it is long, refinancing may not be worth it.

Benefits Of Knowing Your Break Even

Knowing your break-even point helps avoid costly refinancing mistakes. This point shows how long it takes to recover the costs of refinancing. Paying attention to interest rates, loan terms, and closing costs can save money.

Maximizing long-term savings means refinancing only when it makes financial sense. If monthly savings cover the refinance costs quickly, refinancing is smart. Otherwise, it might cost more in the end.

Using a refinance break-even calculator makes this process easy. It divides total closing costs by monthly savings to find the break-even time. This simple step protects from wasting money on bad deals.

When To Refinance For Fast Savings

Refinancing can save money if the interest rate drops enough. A good rule is a rate drop of at least 1% to make refinancing worth it. This helps lower your monthly payment and total interest paid.

Choosing the right loan term is also key. Shorter terms often have higher monthly payments but lower total interest. Longer terms lower monthly payments but cost more in interest over time. Balance your budget with how long you plan to keep the loan.

| Loan Term | Monthly Payment | Total Interest Paid | Best For |

|---|---|---|---|

| 15 years | Higher | Lower | Paying off fast, saving interest |

| 30 years | Lower | Higher | Lower monthly payments |

Common Closing Costs To Consider

Closing costs include many typical fees and charges. These costs affect the total money needed to refinance.

- Loan origination fee: Charged by lenders to process the loan.

- Appraisal fee: Cost for a home value assessment.

- Title search and insurance: Ensures the property has no legal issues.

- Credit report fee: Covers checking your credit history.

- Attorney fees: For legal help during closing.

- Recording fees: Charged by the local government to record the new mortgage.

Strategies to lower closing costs include:

- Shop around and compare lender fees.

- Negotiate fees with your lender.

- Ask the seller to pay some closing costs.

- Choose a no-closing-cost refinance option.

- Bundle fees when possible to save money.

Real Life Examples

Scenario One shows a quick break-even. Closing costs are low, and monthly savings are high. For example, if closing costs are $2,000 and monthly savings are $200, the break-even point is just 10 months. This means you start saving money after less than a year. This option suits those who plan to stay in their home for a short time.

Scenario Two involves a longer break-even period. Closing costs might be $4,000, while monthly savings are $100. The break-even point here is 40 months, or over three years. This works better for homeowners who plan to keep their mortgage longer. They will benefit from the refinance despite the slow start.

Tools And Resources

Several online calculators help figure out the refinance break-even point. These tools ask for details like current loan balance, interest rates, and closing costs. Then, they show how long it will take to recover refinancing costs through monthly savings.

Some popular calculators include:

- Bankrate Mortgage Refinance Break-Even Calculator

- MortgageCalculator.org Refinance Breakeven Calculator

- UMB Bank’s Refinance Break-Even Calculator

- TechCU Loan Refinance Mortgage Calculator

Using these calculators saves time and helps avoid costly refinancing mistakes. Always check the total closing costs and compare them with potential monthly savings. Refinancing only makes sense if you will save money before you plan to sell or pay off your loan.

Keep track of your loan terms and interest rates. This ensures you make smart decisions about refinancing.

Frequently Asked Questions

How To Calculate Refinance Break-even Point?

Calculate the refinance break-even point by dividing total closing costs by monthly savings. This shows how many months to recover refinancing costs.

What Is The 2% Rule For Refinancing?

The 2% rule for refinancing means your monthly savings must equal at least 2% of your loan balance to justify refinancing costs.

How Long Does It Take To Break Even On A Refinance?

It usually takes 12 to 24 months to break even on a refinance. Divide closing costs by monthly savings to calculate your break-even point.

Is It Worth Refinancing From 7% To 6%?

Refinancing from 7% to 6% is worth it if monthly savings exceed closing costs within your planned stay. Calculate your break-even point to decide.

Conclusion

Using a refinance break-even calculator helps you see when savings start. It compares your closing costs with monthly savings clearly. This tool guides smart decisions and avoids costly refinancing mistakes. Knowing your break-even point saves money and time in the long run.

Keep your loan details ready and calculate before you refinance. Simple steps lead to better financial choices for your home.