Looking for the best mortgage deal? Understanding how tracker mortgage rates work can save you thousands over the life of your loan.

But with so many options out there, how do you know which rate is right for you? That’s where a tracker mortgage rate comparison comes in. By comparing current rates side by side, you get a clear picture of what lenders are offering and how it fits your financial goals.

Keep reading to discover how you can make smarter choices, avoid costly mistakes, and find the mortgage rate that truly matches your needs. Your dream home could be closer than you think.

What Are Tracker Mortgages

A tracker mortgage is a type of home loan where the interest rate follows a set base rate. This base rate is usually set by the central bank. The mortgage rate moves up or down in line with this base rate.

Tracker mortgages work by adding a fixed percentage called the margin to the base rate. For example, if the base rate is 3% and the margin is 1%, the total interest rate is 4%. This rate changes whenever the base rate changes.

Key features of tracker mortgages include:

- Variable interest rate tied to the base rate

- Usually no early repayment charges

- Can be cheaper if rates fall

- Monthly payments may change

- Risk of higher payments if rates rise

Benefits Of Tracker Mortgages

Tracker mortgages follow the base interest rate set by the bank or central bank. This means your rate can go down or up with market changes. You can save money if rates drop, unlike fixed rates that stay the same.

Many people like the flexibility of tracker mortgages. You may pay less interest during low rate periods. The rate moves with the market, so your payments can change.

Tracker rates can be lower than fixed rates at the start. But they carry some risk since rates may rise. This makes them a good choice if you expect rates to stay low or fall.

| Feature | Tracker Mortgage | Fixed Rate Mortgage |

|---|---|---|

| Interest Rate | Varies with base rate | Stays the same |

| Monthly Payments | Can increase or decrease | Fixed amount |

| Potential Savings | Yes, if rates fall | No savings if rates drop |

| Risk | Higher if rates rise | Lower risk |

Risks Of Tracker Mortgages

Tracker mortgages follow the interest rate set by the lender’s base rate. This means your interest rate can go up or down over time. When rates rise, your monthly payments increase. That can make budgeting harder and cause financial stress.

On the other hand, if rates fall, your payments may decrease. Still, this is unpredictable. You might pay more than expected if rates climb quickly.

Because of this, tracker mortgages carry risk. They may suit people who can handle payment changes. It is important to understand these fluctuations before choosing this type of mortgage.

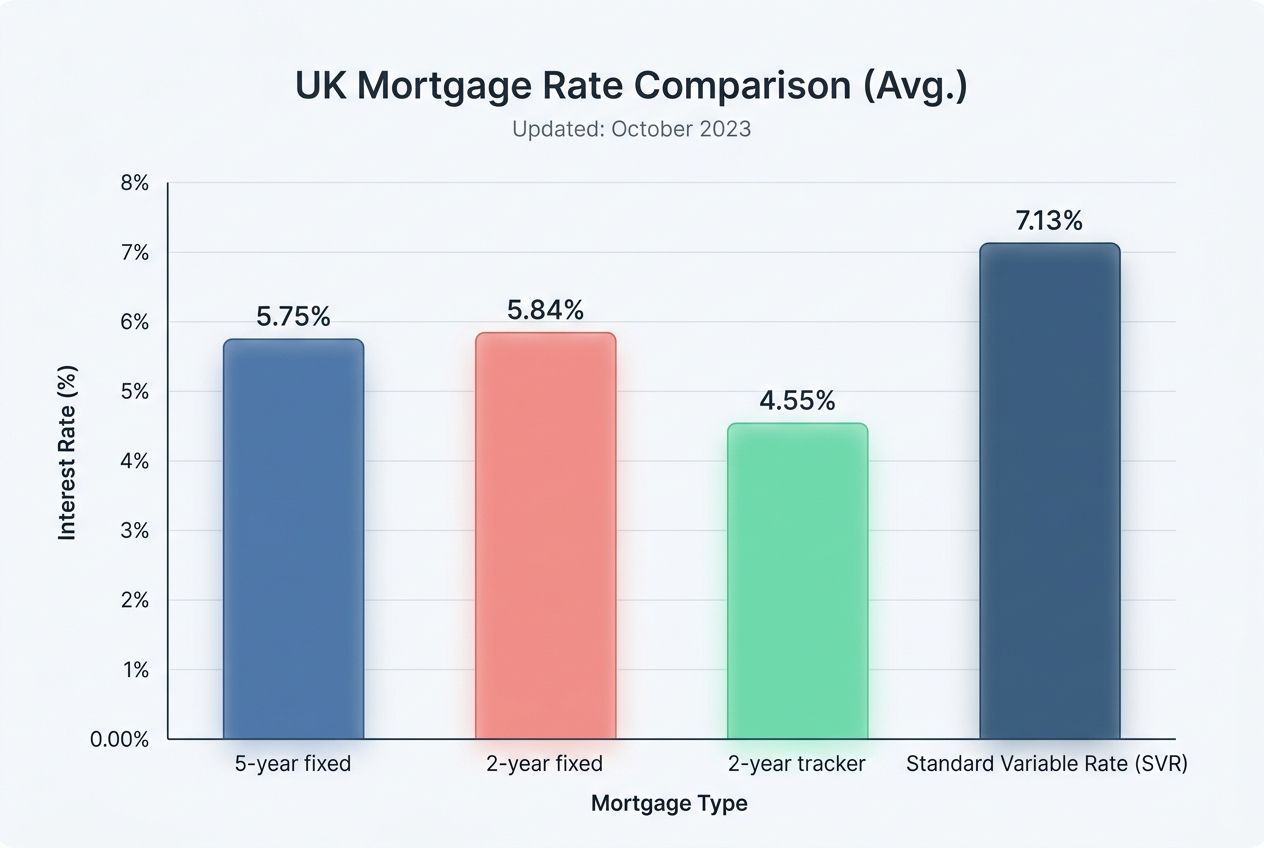

Current Mortgage Rate Trends

Tracker mortgage rates follow the base rate set by the Bank of England. These rates move up or down as the base rate changes. They often start lower than fixed rates, making them attractive for short-term savings.

Fixed rates stay the same for a set period, offering predictable monthly payments. Variable rates can change anytime, depending on the lender’s decisions. Tracker rates are usually more transparent and linked directly to official rates.

| Mortgage Type | Rate Change | Monthly Payment | Risk Level |

|---|---|---|---|

| Tracker Rate | Follows base rate | Varies | Medium |

| Fixed Rate | Stays the same | Fixed | Low |

| Variable Rate | Set by lender | Varies | High |

How To Compare Tracker Mortgage Rates

Online tools help compare tracker mortgage rates quickly. Enter your details once. These tools show rates from many lenders side by side. This helps find the best rate for your needs without calling each lender.

Remember to check more than just the interest rate. Look at fees, loan terms, and early repayment charges. Some lenders may have lower rates but higher fees. Read all terms carefully before choosing.

Watch out for how the tracker rate is set. Some track the base rate plus a fixed margin. Others may change the margin during the loan. This affects your monthly payments.

| Factor | What to Check |

|---|---|

| Interest Rate | Compare current tracker rates from multiple lenders |

| Fees | Look for arrangement fees, valuation fees, and exit fees |

| Loan Terms | Check length, repayment options, and rate change rules |

| Early Repayment | Find out if there are penalties for paying off early |

Top Lenders Offering Tracker Mortgages

National lenders offer a variety of tracker mortgage rates. Some top banks set rates that track the base rate plus a margin. These offers often include fixed fees and no early repayment charges. Popular choices include Bank of America, Wells Fargo, and Chase. They provide wide coverage and competitive rates nationwide.

Local lenders in Austin, Texas often provide personalized service. They may offer flexible terms and lower fees. Examples include Austin Bank and Texas Trust Credit Union. These lenders understand the local market and can tailor mortgage options to your needs.

| Lender | Type | Typical Rate | Special Features |

|---|---|---|---|

| Bank of America | National | Base rate + 0.5% | No early repayment fees |

| Wells Fargo | National | Base rate + 0.45% | Fixed fees, online management |

| Austin Bank | Local (Austin, TX) | Base rate + 0.55% | Personalized service, flexible terms |

| Texas Trust Credit Union | Local (Austin, TX) | Base rate + 0.50% | Lower fees, local expertise |

Using Mortgage Calculators

Mortgage calculators help you estimate monthly payments easily. Enter the loan amount, term, and interest rate. The calculator shows how much you pay every month.

Adjusting for interest rate changes is simple. Change the rate in the calculator to see new payment amounts. This helps plan your budget if rates go up or down.

Track payments over time by entering different interest rates. It gives a clear picture of how your costs may change. This way, you avoid surprises and stay in control.

Tips For Securing The Best Tracker Mortgage Deal

Improving your credit score can lower your mortgage rate. Pay bills on time and keep debts low. Check your credit report for errors and fix them quickly. A higher credit score shows lenders you are reliable.

Negotiating with lenders helps secure better deals. Compare offers from different lenders before choosing. Ask if they can lower fees or interest rates. Explain your good credit and stable income. Small savings add up over time.

When To Choose A Tracker Mortgage

Tracker mortgages follow the base interest rate set by the central bank. They work best when rates are expected to stay low or fall. This means monthly payments can be lower than fixed-rate mortgages. Ideal market conditions include stable or falling interest rates. Rising rates can increase monthly costs quickly.

Personal finances also matter. Choose a tracker mortgage if you have a stable income and can handle some payment changes. It suits people who plan to sell or refinance soon, avoiding long-term risks. Those with tight budgets might struggle if rates rise.

Alternatives To Tracker Mortgages

Fixed-rate mortgages offer a set interest rate for the entire loan period. This means your monthly payments stay the same. It helps with budgeting and avoids surprises if rates rise. Usually, fixed rates start higher than tracker mortgages but give more stability.

Standard variable rate (SVR) mortgages have interest rates that can change anytime. The lender controls the rate, which may go up or down. Payments can be unpredictable, but sometimes rates drop, lowering your monthly cost. SVR mortgages often follow the Bank of England base rate, but lenders can change rates independently.

Frequently Asked Questions

What Is The Best Mortgage Rate Available Right Now?

The best mortgage rate right now varies by lender and credit profile. Current averages range around 6% for 30-year fixed loans. Check trusted sites like Bankrate or NerdWallet for personalized, up-to-date offers. Rates fluctuate daily, so compare multiple sources before deciding.

Is A Tracker Mortgage A Good Idea Right Now?

A tracker mortgage can be risky now due to rising interest rates. It suits those who can handle payment fluctuations. Compare rates and consider fixed options for stability.

What Is The 2% Rule For Refinancing?

The 2% rule for refinancing means your new loan’s interest rate should be at least 2% lower than your current rate. This helps ensure refinancing saves money after costs.

What Is The 3 7 3 Rule In Mortgage?

The 3-7-3 rule means you can refinance your mortgage after three years, pay it off by seven, and the lender has three days to process your application.

Conclusion

Comparing tracker mortgage rates helps you find the best deal fast. Rates can change often, so check regularly. Understand how tracker rates link to the base rate. This helps you predict future payments better. Always consider your budget and financial goals carefully.

Use comparison tools to see different lenders’ offers clearly. Choosing the right tracker mortgage can save you money. Stay informed and take control of your home loan decisions.